A dispute (chargeback) happens when a customer contacts their bank to reverse a payment instead of asking you for a refund. As Merchant of Record, Pandabase receives the dispute from the card network and forwards it to you to respond. You have 7 days from when a dispute is opened to submit evidence. We’ll email you as soon as one is filed.Documentation Index

Fetch the complete documentation index at: https://docs.pandabase.io/llms.txt

Use this file to discover all available pages before exploring further.

Lifecycle

Opened

Order moves to

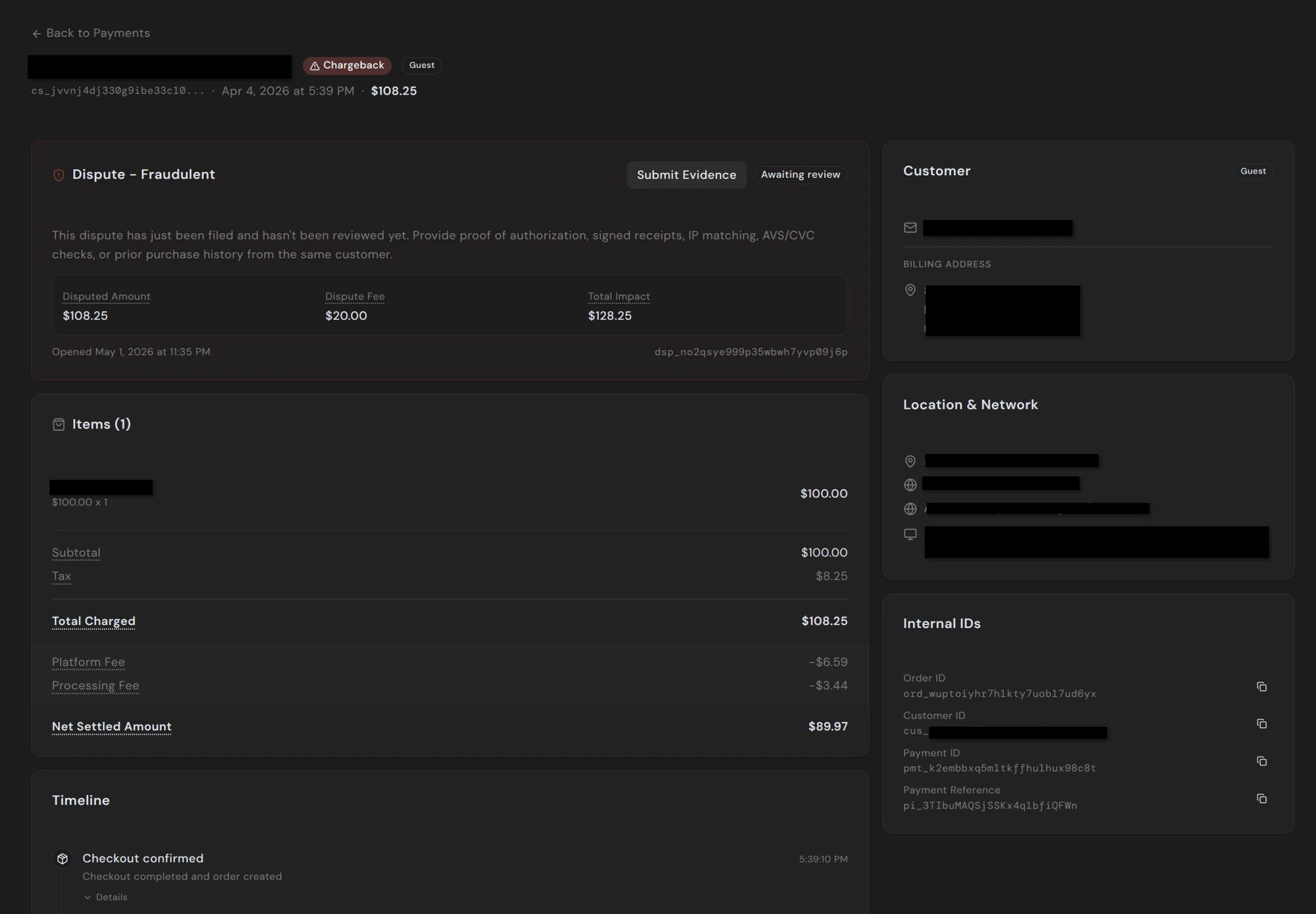

Chargeback. Disputed amount plus a $20.00 dispute fee is deducted from your available balance.Reasons

| Reason | What it means |

|---|---|

| Fraudulent | The cardholder claims they didn’t authorize the charge. |

| Product not received | Customer says they never got what they paid for. |

| Product unacceptable | Received but doesn’t match the description. |

| Subscription cancelled | Customer says they cancelled but were billed anyway. |

| Duplicate | Customer believes they were charged twice. |

| Credit not processed | You promised a refund and the customer never received it. |

| General | No specific reason given by the issuing bank. |

Fees

| Outcome | Effect |

|---|---|

| Dispute opened | Disputed amount + $20.00 fee deducted from your available balance. |

| Won | Disputed amount and dispute fee restored to your balance. |

| Lost | Deduction stands. Original processing and platform fees are not refunded. |

Dispute rate

We expect stores to stay below 0.75% disputes over a rolling 3-month window. Sustained rates above 0.75% lead to outreach from us, additional review on new payments, and — if it doesn’t come down — restrictions or loss of card acceptance. You can see your current rate on the Analytics page.Respond

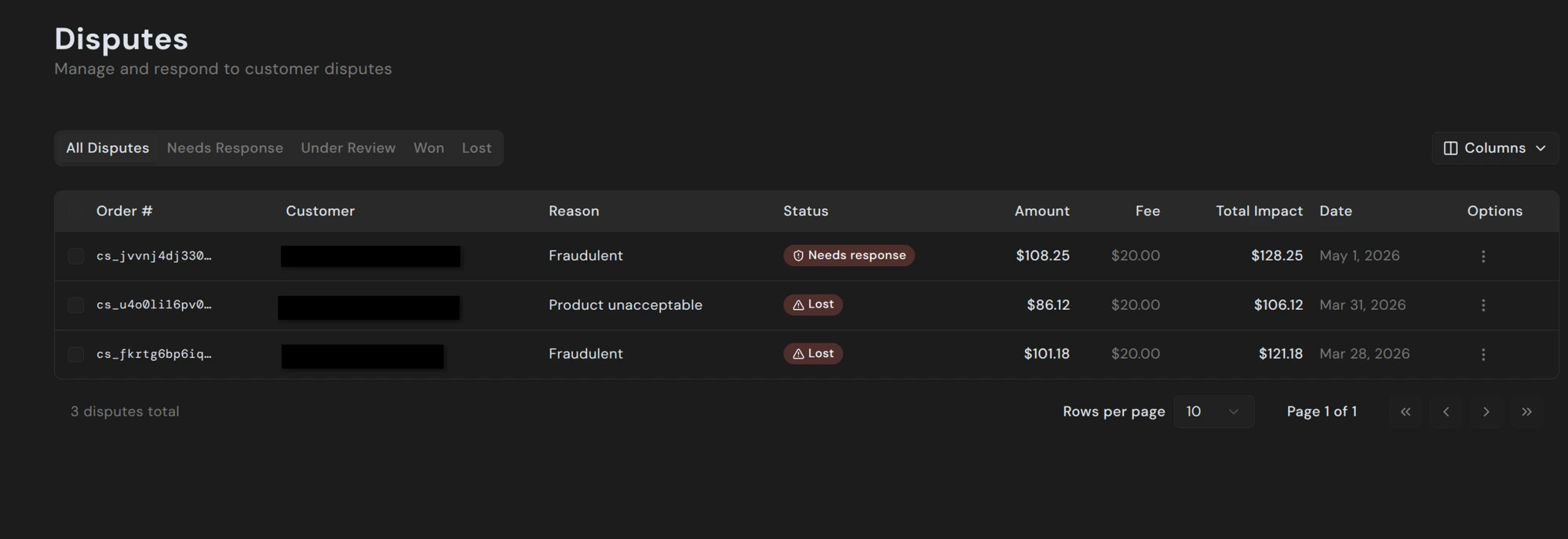

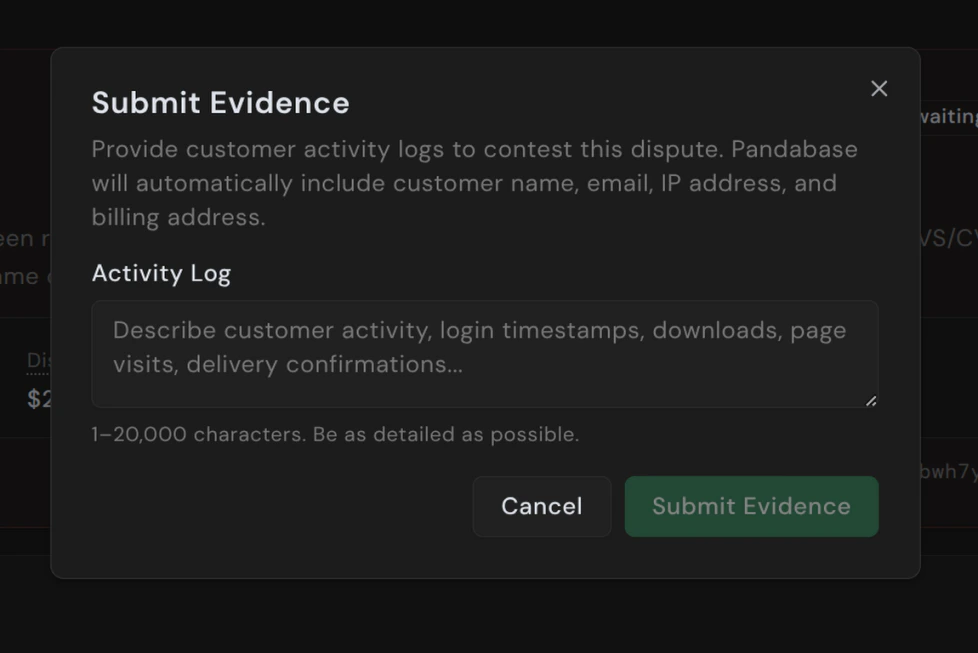

Open the disputed order from the Disputes page. The detail view shows the dispute reason, disputed amount, dispute fee, total impact on your balance, the original order items, customer info, and the full payment timeline.

- Login timestamps, session durations, IP addresses they accessed your platform from

- Downloads, license activations, API calls, content viewed

- Delivery confirmations, support tickets, emails or chats with the customer

- For “product unacceptable”, what was delivered and how it matched the description

- For “subscription cancelled”, proof of continued usage after the alleged cancellation date

Accepting a dispute

There’s no “Accept” button. If you don’t want to fight a dispute, just don’t submit evidence — once the 7-day window closes, the chargeback finalizes against you. The disputed funds and fee stay deducted.Prevention

Pandabase prevents most disputes before they reach you. All of the following run automatically — there’s nothing to configure.Always-on 3D Secure

Every card payment is authenticated with 3D Secure 2 at checkout. If the cardholder can’t authenticate, the transaction is rejected. Successful 3DS shifts liability for fraud disputes from you to the issuing bank in nearly every region we operate.Order Insight & Consumer Clarity

When a cardholder questions a charge with their bank, the bank pulls rich order details (product, merchant name, billing address, fulfillment info) directly from Pandabase. Most “I don’t recognize this charge” disputes resolve here.Early Fraud Warnings

Through our integrations with Verifi (Visa) and Ethoca (Mastercard), the network sometimes tells us a payment is likely to be disputed before the chargeback is filed.- Orders ≤ $50 — refunded automatically. No dispute fee, no impact on your dispute rate, fulfillment revoked.

- Orders > $50 — you decide whether to refund pre-emptively or contest. We email you with the EFW reason.

Compelling Evidence 3.0

For fraud-coded disputes, Pandabase automatically submits a CE 3.0 package when the data supports it. CE 3.0 lets merchants defeat fraud disputes by proving a prior good relationship — we look for two or more prior undisputed transactions from the same cardholder with matching IP, device fingerprint, billing address, or customer account.CE 3.0 has a high win rate but doesn’t apply to every dispute. Disputes where the network confirms the card was used without authorization will be lost regardless of any evidence submitted.

What you can do

- Use a clear store name and product descriptions. Most “fraudulent” disputes are customers not recognizing the charge.

- Make refunds easy. Most disputes start because the customer couldn’t get a response from you.

- Send fulfillment confirmations promptly — receipt and access details in the same email.

- Turn on Pandabase Shield (beta) to auto-decline high-risk payments at checkout.